Please note: Though this post talks specifically about a home loan, it is applicable to any type of loan. I only speak of a ‘home’ loan as I have experience there. Please note #2: All the calculations that you see below have been made by the super-awesome Home Loan Schedule calculator that I wrote a few years ago and something you should check out and bookmark.

So, you have gone ahead and taken a home loan and are looking dejectedly at your bank balance which will never see the highs that it had – just before you put the 20% upfront (required in India). Don’t worry - we have all been there. I have some good news though - things will get better after a while :) I will try to share some insights and tips that I learnt while we tackled our home loan. Recently, while speaking to some friends regarding their loans, I realised how uncommon this knowledge is - so decided to write a post and share what I know.

Some jargon that will be used in the post

- ROI - Rate of Interest (the interest rate that you are paying).

- Principal - The amount of money you require the loan for.

- EMI - Equated monthly installments - the amount of money that you need to pay back to the bank every month.

- Part payment - An amount of money that you pay off more than the required EMI.

- Pre-payment - The amount you pay and the process of closing of the loan by making a final lumpsum amount which equals to the balance principal amount to be paid.

Things to keep in mind BEFORE you take your loan

Everyone will offer you more or less the same interest rates today - but some have better features than others. So always look around and find the institution that has features which will make your life convenient. During our time, Axis bank had no pre-payment charges and was okay with you moving your loan to another bank at no additional cost. All other institutions will charge you a 2% penalty when you try and switch your loan to someone else. ICICI Bank (with whom we ended up going) provides a nifty feature by which you can call them over the phone and make a part-payment every month in under 10 minutes (up to a certain amount). This saves you the hassle of going to the bank and sitting across a person who will take 30 minutes to do the same if you are lucky. SBI always has the best rate of interest but I have found dealing with them to be extremely tedious and something I have really avoided since my college days (I had a student loan with them at the time). So look around and see what features you will require. Remember that you can always negotiate your terms with the banks even if they are not part of the normal plan as the banks are quite desperate to hand out loans to people with good credit rating.

Banks versus other Financial Institutions

Please keep in mind that there are many places were you can get loans. These generally come under 2 categories - banks and home-loan institutions. Examples of banks will be ICICI, Axis, SBI, PNB, etc. Examples of institutions are LIC, India Bulls Home Loan, Reliance Home Finance, HDFC, etc. As a caveat, remember that even though HDFC has banks, its home loan department is a separate entity and does not come under a bank. When we were taking a loan back in 2010/11, different rules governed banks and institutions when it came to loans and we decided to focus on banks as the rules seemed more transparent and governed heavily by the RBI. Please keep this in mind and do your home work. Financial institutions like LIC, HDFC, etc (from experiences shared with me), tend to be less transparent with their interest rates.

Will the Rate of Interest go up or down?

Hmm… When we took our home loan, we were paying 11.5% (which was the standard at the time). At the time of writing this post, my friends are taking loans at 9.4 - 9.5% What my loan advisor explained to me was that even though 11.5% was on the higher end at that time, the good news was that it would go only lower. It all depends on the economy and the growth rate. So, expect your loan to fluctuate between 9% to 12% depending on how we are doing as a country. There was a time when ICICI was offering loans at 7% and I have heard of rates going as high as 14% - but I feel those days are behind us. With so many people buying houses now and RBI playing big-brother, things seem to have settled down. How much does a 2% change in the interest rate affect you?

- Loan of Rs. 50L over 20 years (240 months) @ 9.5% ROI = Rs. 46,606.56 per month

- Loan of Rs. 50L over 20 years (240 months) @ 11.5% ROI = Rs. 53,321.48 per month

So you effectively pay Rs. 6,715 every month for a 2% increase

How loans work?

Apart from the simple principle in which you borrow money from the bank and pay that and some more back, home loans work in a peculiar way when you start repaying the monthly installments.

Banks will always try and recover the interest component of their loans first.

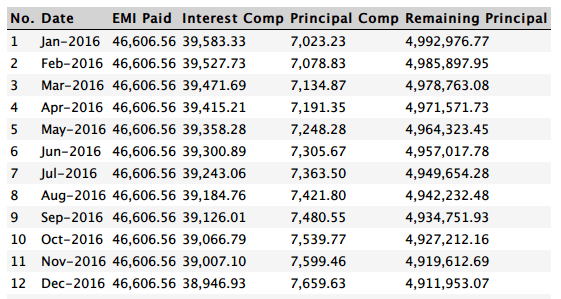

To see what is really going on, you need to take a look at your amortization schedule. Say for example, you are taking a loan as follows:

- Loan Amount: Rs. 50,00,000 (50 lacs)

- Rate of Interest: 9.5%

- Tenure: 20 years (or 240 months) - the standard tenure nowadays

- Start Date: 1-Jan-2016

This works out to an EMI of Rs. 46,606.56 If you will look at your amortization schedule, it will look like this:

As you can see, the bulk of your installment goes into the interest component. So after 1 year, you have paid the bank Rs. 5,59,278 but the actual loan amount paid is Rs. 88,046.94 (16% of the amount paid). The rest of the money or Rs. 4,71,231.78 (84% of the amount paid) goes as the interest component to the bank and does not help in reducing the loan amount. So at the end of year 1, you have paid the bank close to Rs. 5.6L but your loan has reduced only by Rs. 88K If you go down further and see how your year 5 looks like, there isn’t much improvement.

- You pay: Rs. 5,59,278

- Interest: Rs. 4,30,721 (77% of amount paid)

- Principal: Rs. 1,28,557 (23% of amount paid)

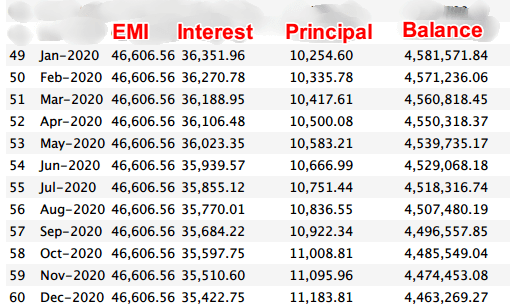

Total paid at the end of 5 years / 60 installments is:

- You pay: Rs. 27,96,390 (~ 55% of your home loan amount)

- Interest: Rs. 22,59,662.83 (81% of amount paid)

- Principal: Rs. 5,36,730.74 (19% of amount paid)

- Load pending: Rs. 44,63,269.26 (89% of the home loan amount taken)

That means if after 5 years of paying the loan, you win a lottery and decide to pay back your 50L loan, you will still have to pay Rs. 44.6L to the bank. So how much do you actually end up paying the bank over 20 years?

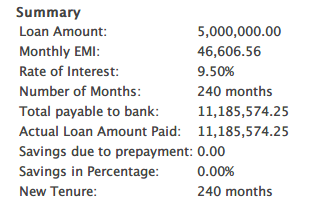

Rs. 1,11,85,574.25 Or Rs. 1.11 Crores on a Rs. 50L over 20 years!

How do I beat this thing?

There is a very simple way to beat this and unfortunately, this is not very common knowledge. This is the most important bit - so read carefully. The biggest damage that you can do to your loan is in the first few years while the interest component percentage is at the highest. As time goes by, this tends to get less and less effective.

Option 1: Increase your EMI

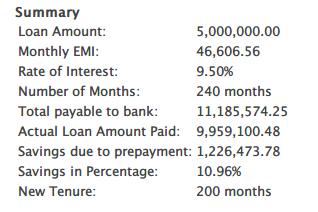

Once you have paid your first monthly installment, head over to the bank and ask them to bump up your EMI to whatever you can afford. I’ll show you a simple example of how this will have an effect. From our earlier example of a Rs. 50L loan / 20 years @9.5%, the EMI comes to Rs. 46,606. If you can even afford to pay Rs. 50,000 - i.e. approximately Rs. 3,400 more from month #2 onwards, this happens:

Your tenure is reduced from 240 months -> 200 months That is, 40 months are shaved off your home loan and you are now paying the bank a total of Rs. 99.6L (approx) versus Rs. 1.11 Crores earlier. A saving of Rs. 12.26L overall or 11% If you say you can afford to pay a little more - say Rs. 55K (instead of Rs. 50K), this is what happens:

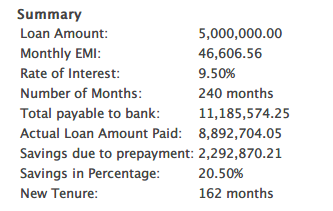

Your tenure is reduced from 240 months -> 162 months and you pay the bank Rs. 88L instead of 1.11 Crore and save a whopping Rs. 22.9L in the process (20.50%)

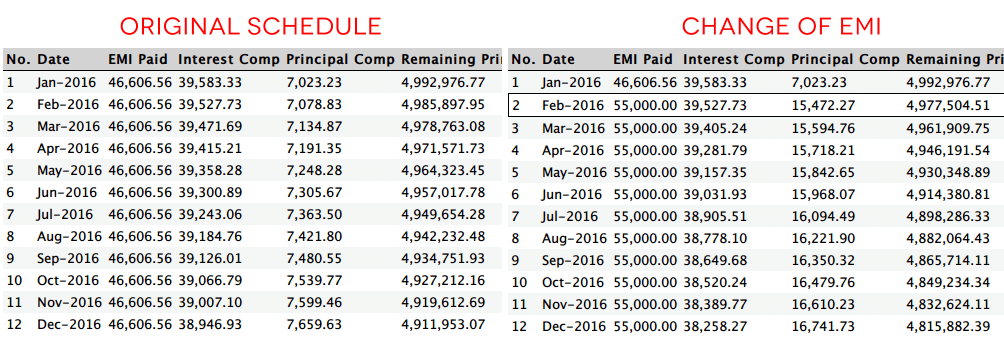

How does this work? If you compare the original payment schedule and the new one, can you spot the difference?

(click for a larger image)

(click for a larger image)

Basically any excess that you pay over your existing EMI, goes directly to your principal. So where earlier, you were paying only Rs. 7,000 odd per month against your principal, you are now paying Rs. 15,000 which really eats up your principal and reduces the interest and hence the tenure. This is the magic of compounding interest and how you can use it to your advantage.

Option 2: Make part-payments

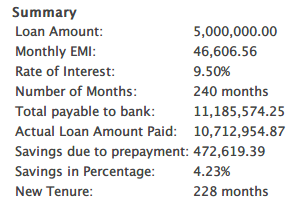

Some banks allow you to make part-payments which are equivalent to one month’s EMI or more while others have no such restriction. (You should find out what your bank’s policy is.) So whenever you are able to save up some money, put it in the loan. It REALLY helps killing that loan off. Say you are able to save up Rs. 1L at the end of the year and you make a part-payment. What happens?

As you can see, making a part-payment of Rs. 1L in month #13, cuts down your tenure from 240 months to 228 months. A saving of 12 months of paying EMIs or basically Rs. 4.72L by paying 1L earlier. Hence, in addition to increasing your EMI, if you make part-payments, that really helps in killing your loan.

Should I save up for part-payments or increase my EMI?

Say for example, you can save 1L additional every year. Does it make sense to part-pay 1L at the end of the year or increase your EMI by Rs. 5K?

It definitely helps to increase your EMI as the extra money you pay cuts into the principal every month and the compounding principal helps you pay lesser every month compared to waiting for 12 months and then making a lumpsum payment.

However, the goal is to do either or both. Whatever you can afford. It does not matter as long as you are making some kind of additional payments.

Reduction in tenure versus EMI?

Whenever you make a part-payment, the bank will ask you whether you want a reduction in EMI or in tenure.

It is ALWAYS better to ask for a reduction in tenure.

Reduction in EMI will keep giving the bank interest for extended periods of time and is not beneficial to your cause at all.

However, there may be some special circumstances under which you would want to reduce your EMI for some temporary relief.

In those cases, after making a part-payment, you can ask your bank for a reduction in EMI. However, this should be the exception rather than the norm.

Some final notes

Every bank is different and they have their own weird clauses. So if you want to follow any advice from this blog, I would highly recommend checking up with your bank first. There could be a clause that you cannot reduce your EMI once you increase it to some level or that you cannot make part-payments for the first year, etc. You have to do your homework and spend sometime with customer care to get your doubts cleared.

Some Examples

The following Google Sheet contains examples of the following:

- Schedule for 20 years with no part-payments

- Schedule for 20 years with increase in EMI to realistic levels (depending on job promotions, etc)

- Schedule for 20 years with part-payments

- Schedule for a non-aggressive, realistic home loan payment (increase in EMI and part-payment)

Spreadsheet: https://goo.gl/qcyPLn

The Calculator

After learning about the amortization schedules and the way this works, I wrote a calculator to help myself with this.

You can find it here: http://calculatehomeloaninterest.com/

I would highly recommend you play with it and find your own sweet spot. If you stumble upon any errors, please do let me know (though I have verified the calculations with my banks schedule and they match up). The table generated can easily be COPY-PASTED into excel for further analysis, etc. Hoping this post has been useful to you.

Happy home-loan-hacking!